Here’s a retirement planning tip for 2021: Think of your retirement savings plan as a ship passing through ocean waves. You are the captain. And it’s your job to keep that ship off shoals that could sink it. It’s your job to avoid nasty currents that can delay its progress.

How can you do your job? You make one important decision after another.

Here are five such decisions you could face in 2021. Here’s how to handle them, with advice from leading financial advisors.

2021 Retirement Savings Must-Do Decision #1: Time To Create Your Investment Plan?

Whatever your retirement savings goal is — $500,000, $1 million, more? — once you figure out how much you need, you must decide how to reach that savings goal.

That means deciding which types of investments to use. If you haven’t already made that decision, it’s vital to do it now.

In your 401(k) account, you likely only have access to mutual funds. Keep in mind you don’t need to limit yourself to your 401(k) and IRAs for your retirement savings. But let’s assume you only use mutual funds or exchange traded funds (ETFs) in your 401(k) and IRAs.

While you are young, you should rely heavily on stock funds because those give you the compound growth you need. “Young investors have time to benefit from rallies and rebounds,” said Judith Ward, a senior financial planner for mutual funds powerhouse T. Rowe Price (TROW).

Investors up to age 50 with high risk tolerance and no current need to tap their retirement savings accounts for cash can even be 100% invested in stock funds, Ward says.

Beyond that age, how much in stock funds? Try an updated version of an old rule of thumb: subtract your age from 120. The result is the percent of stock funds that an average investor needs. If you’re 65, for example, you need 55% of your retirement savings in stocks and stock funds.

To fine tune your stock fund allocations among categories such as U.S. vs. foreign and various sectors, check out allocations in target date funds that you like, whose target dates match your retirement year.

As for the portion of your overall portfolio that uses individual stocks, your choices and buy-sell decisions should be based on the time-tested CAN-SLIM strategy.

2021 Must-Do Decision #2: Time To Rebalance?

Despite the tumult of 2020, the market did well. The S&P 500 was up 15.3% through Dec. 1.

But what if that strong performance threw your investment plan out of whack? Suppose your plan dictates that, at your age, you have a 90% allocation to stock funds. Of that, suppose you want 70 percentage points in U.S. stocks, 15 points in emerging markets and the balance in high-yield dividend stocks.

But what if, come Dec. 31, your asset mix has deviated from your plan? “Time to rebalance,” Ward said. Either reallocate money among funds inside your retirement savings accounts. Or change allocations of 2021 contributions to restore your planned asset mix.

2021 Must-Do Decision #3: Need To Make RMDs In 2021?

Required minimum distributions (RMDs) are withdrawals that retirees must start to take from their traditional IRA and 401(k) accounts.

The Secure Act pushed back the starting age for RMDs to 72 from 70-1/2 as of Jan. 1, 2020. The new starting age applies to anyone born on or after July 1, 1949. For older investors, 70-1/2 remains the RMD starting age.

But last March, the Cares Act waived RMDs for calendar 2020.

That delay lets your retirement savings account balances grow longer without being whittled down by income taxes on withdrawals.

Still, delaying RMDs is helpful only if you can afford to do without the income.

In any case, don’t forget that RMDs resume in 2021. Failure to take RMDs on time results in a whopping 50% penalty plus income tax.

2021 Retirement Savings Must-Do Decision #4: Should You Make A Roth Conversion?

Sure, the market was up in 2020. But what if you got laid off or lost income? “If you had a low-income year in 2020 or 2021, you should assess whether a Roth conversion makes sense,” Ward said.

If you shift money from a traditional IRA to a Roth IRA (or from a traditional 401(k) to a Roth 401(k)), your future withdrawals from Roth accounts will be tax-free if done properly. The catch is that you must pay income tax on any amounts transferred.

Paying that tax can make sense if your tax bracket and rate fell in 2020 or 2021 due to loss of a job or income. And that happened to millions of Americans because of the coronavirus pandemic.

Triggering a tax bill can still help your retirement savings plan even if you don’t suffer a layoff or lost income in 2020 or 2021. How? Paying tax now makes sense if your tax rate is lower in whichever year, such as 2021, that you transfer money to a Roth account than it will be years from now, once you retire and start to make taxable withdrawals from the account.

2021 Retirement Savings Must-Do Decision #5: Figure Out How To Generate Income

Interest rates remain historically low. That means generating useful income remains a challenge. After all, if you stuck up to $100,000 into a bank savings account, the best rate that you could find in late December was 0.65%, according to depositaccounts.com. And that was from an online bank.

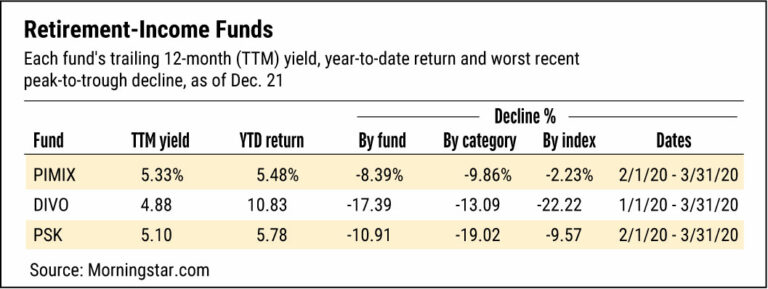

So how can you squeeze income from your cash? The trailing 12-month (TTM) yield from an S&P 500 Index fund like SPDR S&P 500 ETF (SPY) is 1.57% as of Dec. 21. So how can you at least double that, let’s say, without taking on too much risk?

Solutions all involve some risk of volatility. Your principal can lose value in a down market. That’s very unlike cash in a bank savings account.

But leading financial advisors say you ought to consider these securities if you want to at least double the yield provided by the S&P 500. Data are from Morningstar.com.

Pimco Income Fund (PIMIX): “Pimco Income is a go-anywhere bond fund that invests in a range of global fixed-income sectors,” said Andy Kapyrin, co-head of investments, RegentAtlantic. “This approach may help the fund produce returns better than a traditional bond portfolio that looks only at sectors in the Barclays Aggregate Bond Index.”

Amplify CWP Enhanced Dividend Income ETF (DIVO): This fund offers a two-prong approach to income, says Faron Daugs, founder and CEO, Harrison-Wallace Financial Group. It aims for dividends from common stocks. And it seeks income from call option premiums. Covered call options avoid long-maturity bonds, whose values and total returns get torpedoed by rising interest rates. Covered calls also avoid bond-proxy stocks whose share prices get hurt by rising rates. And the strategy avoids high-yield stocks, whose low credit quality and default risk also puts investors in jeopardy.

SPDR Wells Fargo Preferred Stock ETF (PSK): Investing in this fund would provide diversification from bonds. Preferred stock is a hybrid security that pays dividends that are fixed like bond interest. But preferred shares appreciate in value more like common stock than bonds. “Reducing risk in one’s fixed-income allocation allows investors to take risk elsewhere should they want or need to, such as in equities,” said Kelly Ryan, head of Independent Wealth Management at State Street Global Advisors, parent of the SPDR line of ETFs.

Retirement And HSA Plan Annual Contribution Limits

| Contribution Limits: 2020 & 2021 | ||

|---|---|---|

| Type of account | 2020 | 2021 |

| IRA | $6,000 | $6,000 |

| IRA catch-up contribution | $1,000 | $1,000 |

| IRA: nonworking spouse contribution | $6,000 | $6,000 |

| SEP IRA | lower of 25% of your compensation or $57,000 | lower of 25% of your compensation or $58,000 |

| 401(k) | $19,500 | $19,500 |

| 401(k) catch-up contribution | $6,500 | $6,500 |

| Health savings account (HSA) family coverage | $7,100 | $7,200 |

| Health savings account (HSA) individual coverage | $3,550 | $3,600 |

| Health savings account (HSA) catch-up contribution | $1,000 | $1,000 |

– Paul Katzeff| investors.com